دعونا نتحدث عن العقود المستقبلية للأسهم المفردة

أطلقت السوق المالية السعودية (تداول) الشهر الماضي العقود المستقبلية للأسهم المفردة (SSF)، ويعد هذا الإطلاق الثاني ضمن سلسلة من منتجات المشتقات المالية التي سيتم طرحها في سوق الأسهم السعودية. تتم هذه الإضافة الجديدة على بعد عامين من إطلاق مؤشر العقود المستقبلية MT30)) والذي كان أول منتج مشتق متداول في سوق الأسهم السعودية. تنويع فئات الأصول المتاحة للمستثمرين في أسواق المال هو أحد الأهداف الرئيسية للقطاع المالي في البلاد. وعلى هذا النحو، فإن إطلاق المشتقات المالية يمكن أن يلعب دورا أساسيا في تحقيق هذا المسعى. فهي توفر أداة فعالة لإدارة المخاطر، وتوسع المنتجات المتاحة للتداول، وتعزز شفافية التسعير، وتدعم كفاءة سوق رأس المال بشكل عام.

كما يعلم الكثير منكم، فإن العقد المستقبلي هو اتفاق ملزم قانونا بين طرفين، حيث يتفق الطرفان على شراء أو بيع أصل معين بكمية محددة في تاريخ محدد مسبقا في المستقبل وبسعر ثابت محدد مسبقا. على عكس العقود المستقبلية لمؤشر MT30 التي تستمد قيمتها من مؤشر أساسي، ترتكز SSF إلى الأسهم المفردة. وستستند الشريحة الأولى من المنتج إلى عشر شركات مدرجة لتداول العقود المستقبلية عليها. وقد جرى في اختيار الأسهم التي تتخذها العقود المستقبلية للأسهم المفردة كأصل أساسي لها عوامل نموذجية مثل القيمة السوقية والسيولة، لضمان نشاط تداول كاف في سوق ال SSF. يحتوي كل عقد على 100 سهم ويتم تمويل هذه الصفقات عن طريق إيداع هامش أولي. يتم تحديد الهامش الأولي (عموما حوالي 20٪ من القيمة النقدية الإجمالية للأسهم) من قبل شركة مركز مقاصة الأوراق المالية (مقاصة) بناء على التقلبات المحتملة للأصل الأساسي وتصنيف المستثمر.

الجدير بالذكر أنه بعد عدد من إصلاحات السوق المالية في العامين الماضيين، تم إدراج سوق الأسهم السعودية بنجاح في المؤشرات العالمية الرئيسية مثل FTSE Russel و S&P DJI للأسواق الناشئة. ومنذ ذلك الحين، تم جذب المزيد من الاستثمارات الأجنبية، وبالتالي إطلاق نوع جديد من المشتقات يبدو كخطوة منطقية تالية نحو تعزيز نطاق المستثمرين المؤسسيين المحليين والأجانب في إدارة مخاطر السوق والحفاظ على التعرض المستهدف لمعايير أداء الاستثمار. وبلا شك، فإن مثل هذه الإضافة بإمكانها أن تضفي مزيدا من العمق لواحدة من أكبر أسواق الأوراق المالية في المنطقة.

نظرة عامة في المؤلفات

يعتمد تأثير تداول المشتقات على أسواق الأسهم على العديد من العوامل. وتشمل تلك العوامل الهيكل التنظيمي، وآلية التداول والبنية التحتية، وتصميم العقود المستقبلية، ووقت إطلاق المشتقات في السوق. فاستدلالات بعض المؤلفات حول تأثير SSF والمشتقات المالية بشكل عام على الأصول الأساسية (السوق الفورية للأسهم) متفاوتة نوعًا ما.

من حيث تقلبات الأسعار، لا يبدو أن إطلاق تداول العقود المستقبلية للأسهم المفردة يؤثر على تقلبات نظيرتها الأساسية. في الواقع، انخفضت تقلبات الأسعار الأساسية من خلال الفحص التجريبي في أسواق مثل تايلاند وروسيا بعد إدراج تلك العقود المستقبلية. أما بالنسبة لقدرتها على اكتشاف الأسعار، فإن الأدلة التجريبية الداعمة والمتعلقة بدور المشتقات بشكل عام على عكس المعلومات الجديدة في أسعار الأصول الأساسية موثقة توثيقا جيدا. مما يشير إلى أن الأسعار في سوق المشتقات تقود الأسعار في السوق الفورية لأنها تعكس المعلومات الجديدة بشكل أكثر كفاءة. ومع ذلك، لا يوجد إجماع كامل بين الباحثين حول هذا الدور وذلك بسبب بعض النتائج المتضاربة أو غير الحاسمة التي تنطوي على اتجاه وتقلب ووتيرة تدفق المعلومات بين السوقين.

ماذا عن السيولة؟ كان هناك قدر كبير من النقاش حول تأثير المشتقات على سيولة الأصول الأساسية. ففي أسواق مثل الولايات المتحدة، أشارت العديد من الدراسات إلى وجود علاقة إيجابية بين إدراج المشتقات وأحجام تداول الأصول الأساسية من خلال الفحص الإحصائي لأحجام التداول قبل وبعد إدراج المشتقات. من ناحية أخرى، في سوق مثل ماليزيا، لا يبدو أن إدراج SSF يؤثر على مستويات السيولة في السوق الفورية. أما في الهند، فتشير بعض الدراسات إلى أنه كان له تأثير سلبي ناشئ عن تحول أنشطة المضاربة من السوق الفورية إلى سوق المشتقات.

وبغض النظر عن تأثيرها على السوق الفورية، هناك ما يكفي من الأدلة في المؤلفات التي تشير إلى أن أسواق المشتقات تميل إلى جذب المتداولين المطلعين – سواء كان ذلك للتحوط، أو المراجحة، أو المضاربة. ولم لا إذا كانت توفر تكلفة أقل للصفقات، ومتطلبات مالية مقدمة أقل، وكذلك قيود أقل للتداول. عندما يتعلق الأمر ب SSF، فإن قدرتها على هيكلة استراتيجية ترتكز على أسهم شركة فردية واحدة وتقديم رافعة مالية بالمقارنة مع تداول الأسهم بشكل مباشر تجعلها خيارا جذابا لبعض المتداولين. يمكنها أيضا أن تقدم بديلا لائقا للمتداولين للبيع على المكشوف. يحدث البيع على المكشوف عندما يقترض المتداول ورقة مالية ويبيعها في السوق المفتوحة، ويخطط لإعادة شرائها لاحقا بأقل من سعر البيع. وقد نظمت المملكة آلية التداول هذه منذ عام 2017 وتم تعديلها لاحقا في عام 2021. ومع ذلك، لأسباب خارجة عن نطاق هذه المقالة، لم يكن للبيع على المكشوف نشاطا حقيقيا محليا. مع وجود SSF الآن في السوق، يمكن للمتداولين محاكاة الهدف الاقتصادي للبيع على المكشوف بسهولة نسبية وبتكلفة أقل نظرا لعدم وجود بعض الشروط المطلوبة في عمليات البيع على المكشوف.

وبالإضافة الى قدرة SSF على مساعدة مديري الصناديق والمستثمرين المؤسسيين في إدارة محافظهم الاستثمارية وفقا لشهية المخاطر المختلفة لديهم، يمكنها أيضا لعب دور رئيسي في مبادرات المملكة نحو تطوير صناعة صناديق المؤشرات المتداولة (ETF). وعلى الصعيد العالمي، يتم استخدام SSF والعقود المستقبلية للمؤشرات على حد سواء، عادة كأدوات فعالة إما لزيادة الرافعة المالية أو خفضها وتلبية العوائد المطلوبة للمستثمرين. علاوة على ذلك، قد يستخدم مدير صندوق المؤشرات المتداولة المشتقات للتحوط ضد الحركة غير المواتية في السوق الأساسية أو جذب المستثمرين الذين يراهنون ضد اتجاه الأصل الأساسي من خلال الاستثمار فيما يسمى بصناديق المؤشرات المتداولة العكسية.

تجدر الإشارة إلى أن المشتقات بشكل عام، وSSF بشكل خاص، محفوفة بالمخاطر بطبيعتها. ومن هنا يجب أن يدرك المتداولون والمستثمرون أن خطر الخسارة قد يتعدى بكثير حجم الاستثمار الأولي، وبالتالي يتطلب التعامل مع المشتقات المالية اليقظة. يتم حساب القيمة العادلة على المراكز المفتوحة في السوق يوميا، وإمكانية حصول المتداول على إشعار من الوسيط يطلب منه رفع مستوى الهامش المبدئي أمر وارد جدا ولابد أن يؤخذ بالاعتبار. عند التعامل بعقود SSF، من المهم ايضا النظر إلى مستوى تقلبات السهم الأساسي وذلك لارتباطه بشكل مباشر مع تقلبات مراكز العقود المستقبلية المفتوحة للمتداول. علاوة على ذلك، فإن مستويات السيولة للأداة المستقبلية المختارة هي ذات أهمية قصوى. يمكن أن تظهر الأدوات منخفضة السيولة تفاوتات مفرطة في الأسعار، وبالتالي، يمكن أن تكون محددا رئيسيا في نجاح أو فشل استراتيجية التداول او التحوط.

التجربة حتى الآن

منذ إطلاقها في أغسطس 2020، استقطبت العقود المستقبلية لمؤشر MT30 سيولة متواضعة على أقل تقدير. وبناء على تصريحات إعلامية من الرئيس التنفيذي لشركة تداول، تم تداول أكثر من 500 عقد بقيمة إجمالية بلغت 150 مليون ريال سعودي. كما سلط الضوء على المقاصد الاستراتيجية وراء الإطلاق وأنه يستهدف مجموعة محددة من المستثمرين الدوليين الذين يتبعون مؤشر ال MSCI. من خلال النظر إلى أسواق مماثلة، فإن القيمة الافتراضية الإجمالية للمشتقات عادة ما تساوي أو تتجاوز قيمة التداول في سوق الأسهم. وقد بلغ إجمالي قيمة التداول في سوق الأسهم السعودية 2.24 تريليون ريال سعودي في عام 2021م. وبالتالي، فأنه من الإنصاف القول إن مسار المملكة نحو الوصول إلى مستوى يماثل النظراء من حيث أحجام التداول لا يزال بعيدا وغير واضح.

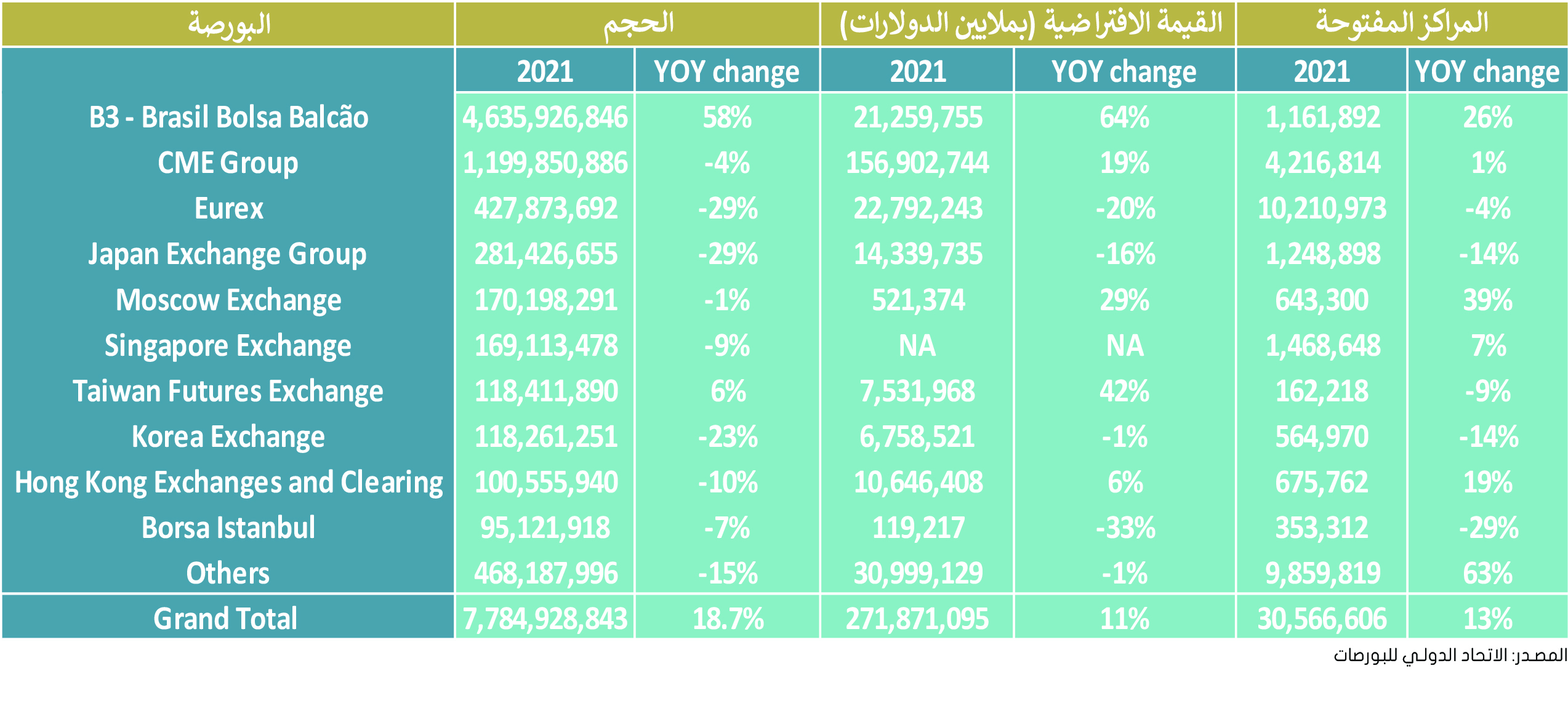

وعلى الرغم من ذلك، فمن المتوقع إلى حد ما أن يكون مستوى السيولة محدود في العام أو العامين الأولين حيث يتعرف المشاركون في السوق على المنتج الجديد ويصل السوق إلى شكل من أشكال النضج. وعلى الصعيد العالمي، يوضح الجدول أدناه المأخوذ من تقرير الاتحاد الدولي للبورصات لعام 2021 عن نشاط المشتقات، أكبر عشر بورصات من حيث عدد العقود المستقبلية المتداولة لمؤشرات الأسهم في عام 2021. عندما يتعلق الأمر بالعقود المستقبلية للمؤشرات، تشكل B3 (بورصة برازيلية) حوالي 60٪ من الحجم العالمي. أما بالنسبة للعقود المستقبلية للمؤشرات الأكثر تداولاً، فقد كان مؤشر E-MINI S&P500 الأكثر نشاطا حيث تم تداول أكثر من 403 ملايين عقد في عام 2021.

حاولت العديد من البورصات في جميع أنحاء العالم إدراج العقود المستقبلية للأسهم المفردة، ولكن لم تنجح جميعها. سيعتمد تطور نشاط التداول وبالتالي السيولة في سوق المشتقات المتداولة المحلية على العديد من العوامل. وفيما يلي قائمة غير حصرية ببعض المحددات الرئيسية:

خصائص الأصول الأساسية والعقود المستقبلية: أظهرت الأسهم ذات الأحجام السوقية الكبيرة والتقلبات السعرية العالية والسيولة العميقة أن لها تأثيرا إيجابيا على نجاح العقد. بالإضافة إلى ذلك، فأن تباين التسعير بشكل منتظم بين الأسواق الفورية والمستقبلية يؤدي الى استمالة المستثمرين المطلعين إلى سوق العقود المستقبلية. إلى جانب ذلك، تساهم عوامل مثل حجم العقد والحركة السعرية وشهور العقد على سهم معين بشكل كبير في زيادة المراكز المفتوحة وحجم التداول. يقترح بعض الباحثين أن تقليص حجم العقد كان له تأثير إيجابي على حجم تداول العقود المستقبلية وساهم بدوره في نجاح العقد المستقبلي. من ناحية أخرى، يمكن أن يكون لتضييق حد التذبذب السعري اليومي تأثير معاكس.

أنواع المستثمرين ومعرفتهم: في سوق يشكل فيه المستثمرون الأفراد نسبة كبيرة من حجم التداولات اليومية، لن يكون من المستغرب أن يعاني هذا السوق من سيولة محدودة في العقود المستقبلية. كما ذكرنا سابقا، عادة ما تجتذب أسواق المشتقات المتداولين/المستثمرين المطلعين، وبالتالي، فإن العقد المستقبلي سينجح نظريا إذا عالج حاجة المستثمرين للتحوط. وهذا يتطلب أن يكون المضاربون المطلعون قادرين على إدارة مخاطر تولي مراكز التحوط تلك. من الناحية الواقعية، فإن امتلاك المعرفة بين مستثمري الأفراد حول سوق العقود المستقبلية والطريقة التي يعمل بها أمر أساسي لنجاحه. بالإضافة إلى ذلك، غموض العقود المستقبلية عند البعض من منظور توافقها مع الشريعة الإسلامية تثبط مجموعة معينة من المستثمرين عن تداولها. وقد يؤدي إتباع نهج إعلامي موجه لمعالجة هذه الفجوة الى استقطاب المزيد من المستثمرين.

صناع السوق والسيولة: سلط العديد من الباحثين الضوء على المهمة الحيوية لصناع السوق في تعزيز السيولة. عادة ما تشكل شركات الوساطة ركيزة أساسية في صناعة السوق، وذلك لأنها تساهم في توفير أسواقا شفافة ثنائية الاتجاه عندما يكون السوق مفتوحا. وحتى لو كانت السيولة وفيرة في أوقات معينة، فإن دورها ملموس في التخفيف من تدهور أسعار الاوراق المالية عندما تكون الأسواق متقلبة والفروق السعرية واسعة النطاق. يوفر صانعو السوق السيولة والعمق الضروريين للأسواق وفي الوقت نفسه يستفيدون من الفروقات السعرية بين العرض والطلب.

يبقى أن نرى ما إذا كانت العقود المستقبلية للأسهم المفردة ستعمل على النحو المنشود في الأشهر والسنوات القادمة. أعتقد أن السوق المالية السعودية (تداول) وكذلك المنظومة المالية بأكملها الداعمة لهذه المبادرة تستحق الثناء على جهودها الرامية إلى النهوض بسوق الأسهم السعودية. وتجدر الإشارة إلى أن إطلاق المشتقات المالية المتداولة في السوق لن يكون ممكنا بدون تطوير الإطار التنظيمي المرتبط به والبنية التحتية ذات الصلة. ليس لدي أدنى شك في أنه مع مرور الوقت، ستعمل هذه الإضافة الأخيرة على تعزيز نمو سوق المشتقات في البلاد لتشمل منتجات إضافية. المرحلة التالية هي الخيارات المتداولة في السوق، وعلى الرغم من أنها قد تكون أصعب من حيث التنفيذ وأعقد من العقود المستقبلية من حيث التداول، إلا أنها على نطاق عالمي، تعتبر الأكثر تداولا من بين منتجات مشتقات الأسهم.

Partner